Bulk Sliced SDCs

Inventory available for prompt shipment and forward contracting.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

Bulk Natural Thompson Seedless raisins and other California raisins are now being packed and shipped from the new crop. We have seen stable prices in recent weeks thanks to a robust California Thompson Seedless Select (NTS) raisin crop with exceptional quality. Compared to this time last year, there were no major rain events during the most important parts of the raisin harvest in California this year. We have seen strong demand from Japan and the APEC countries as we enter the Lunar New Year purchasing period. Although there remains strong demand in much of the APEC region, Chinese buyers are notably hesitant to jump into the market at current prices due, in large part, to anxiety created by the ongoing US / China Trade War.

As for quality, early reports from the fields indicate a robust and delicious 2018 raisin crop; in stark contrast to the innumerable quality issues faced by buyers and suppliers during the 2017 / 2018 harvest season. Many suppliers who make Jumbo and Select size Golden raisins are reporting a shortage of Jumbo Sizes with many unable to offer Jumbo Golden raisins at this time. California’s crop of Jumbo and Select (Medium) Flames looks to be of excellent quality with an average number of Jumbo and Select (Medium) Flame raisin sizes. Prices for California Flame raisins in 2018 are higher than last year thanks to the steadily growing global demand for this delicious raisin. The Raisin Bargaining Administration (RBA) and it’s eleven signatory packers have agreed to a one year price per ton. This will not have much effect on pricing at this stage in the harvest since most packers have already been shipping raisins from the 2018 crop.

We supply all major bulk California raisins including dried-on-the-vine (DOV) and tray-dried Natural Thompson Seedless Selects, Selma Petes, Flames, Goldens, and other varieties in Jumbo, Select, and Midget sizes and welcome your inquiries. We also supply Selma Pete DOV Double-Run Supreme raisins to Japan and elsewhere which are processed twice to achieve exceptionally low stem and capstem counts.

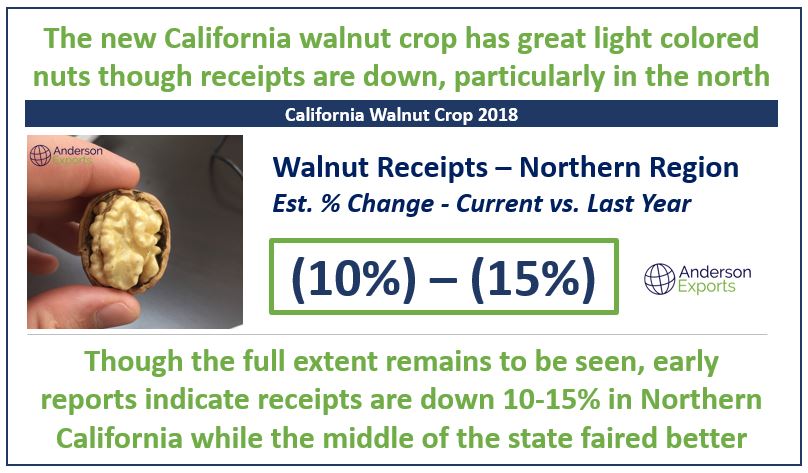

The biggest news in California walnuts this week is the continuous flow of reports from suppliers indicating a shorter than expected Chandler crop in 2018. Suppliers around the state of California are reporting that the Chandler walnut crop is down, especially in the north, where some estimate the crop to be down 10 - 15% compared to last year.

In addition to this shorter crop, many suppliers are observing that Chandler walnuts in general are seeing lower average meat-yields compared to both last year and the 10-year average.

These new revelations will no doubt affect the prices moving forward for in-shell Chandler walnuts. The impact of the shorter Chandler crop, coupled with the lower-than-average meat-yields will remain to be seen as the season progresses. Lower average meat-yields may motivate suppliers to crack out more of their Chandlers, as they can control the final product with high-tech sorting far more than for raw in-shell. The news is not all bad for Chandler walnuts though, the product that has been received from the fields, despite the lower meat-yields, is a gorgeous light milky off-white color.

Many suppliers are reporting good light color and average meat-yields for in-shell Howard walnuts for the 2018 crop. Howards are harvested earlier than Chandler and on average have a higher meat-yield. This makes it a good alternative to Chandler for those buyers who require higher average meat-yields at a more competitive price.

We work with California’s top walnut packers to supply our customers with Jumbo and Jumbo / Large (J/L) in-shell Chandler, Howard, Hartley, Vina, Tulare, Serr and other varieties. We also provide bleached in-shell walnuts in addition to California shelled product including Chandler and non-Chandler Light Halves & Pieces (LHP) 20%, 40%, 80% and higher based on customer requirements.

News from the bogs continues to affirm the possibility of a smaller than expected new cranberry crop. Wisconsin cranberry production is expected to be down and there are some concerns about rot in Massachusetts. Though it is still early to tell, the decrease compared to last year may be in the 12 - 18% range.

Since the cranberry market is already tight on fruit, lower new production may compound the already widespread shortages in the market for Sweetened Dried Cranberries (SDCs). There is also the wildcard of the 25% Producer Allotment (supply reduction) still in play since the USDA has yet to approve the proposal. Current lead times on Whole and Sliced SDCs remain long and prompt shipment loads are few and far between. Given these conditions, we anticipate firm prices with modest increases throughout the year for SDCs.

We supply Conventional and Organic Whole or Sweetened Dried Cranberries (SDCs) packed in bulk cases as well as 50 Brix and 65 Brix cranberry concentrate shipped in bulk 55 gallon drums.

The new California pistachio crop looks excellent though we are seeing size ranges widen as suppliers work to accommodate to the smaller than average nut size coming out of the fields. We are seeing offers on US Ex. #1 21-25 as a 21-26 or even 21-27. The demand for California pistachios dwarfs the supply so we expect tight availability and firm pricing in the year ahead. California is also in an advantaged export position this year relative to Iran due to Trump’s regime of sanctions on the country and the campaign to make it harder to do business with Iran’s counter-parties. Overall, California’s pistachios will be highly sought after so buyers would be prudent to engage early to secure their forward needs.

We are now supplying new crop in-shell and shelled pistachios of all major types and sizes.

China’s apple crop is experiencing major disruption due to crop failure and regulators shutting down apple production facilities due to environmental concerns. We have heard estimates of a crop reduction in the 30 - 35% range and prices are reacting accordingly. Disruptive ripples are flowing downstream to importers who are understandably concerned about how securely their forward apple needs are covered. Some Chinese suppliers are unable to fulfill contracts and others are opting to re-negotiate. Suppliers who will offer may be hesitate to lock a price for 12 months given the volatility.

We are engaging new clients of dehydrated apple dices in the wake of these supply disruptions and are eager to supply dehydrated apple dices with or without sulphur dioxide (SO2) from our BRC supplier in China as well as our suppliers in South America this year. Supply of dehydrated apple dices from South America will not be available until April / May 2019 when the new crop is processed and ready for export. We supply with Granny Smith, Red Delicious and other varieties in dices / cubes of 5 x 5 x 5MM, 10 x 10 x 10MM and other sizes upon request.

We supply Fancy Junior Mammoth Halves (FJMH), Fancy Mammoth Halves, Fancy Pieces, and other sizes / types for all major U.S. pecan varieties.

HONEY (HN 80) - Wildflower Multifloral Bee’s Honey & Honey Powder

100% pure liquid honey (HN 80) Is obtained from the Western Honey Bee (Apis Mellifera) in the region of Campeche, Mexico. This region is recognized worldwide because of the high quality honey that is produced there with flavor that comes from the region’s endemic wildflowers.

COCONUT SUGAR - Organic and Conventional Natural Sweeteners

We have both organic and conventional coconut sugar. Our suppliers of organic coconut sugar are renowned for a product with 99% purity (checked by carbon isotope analyzer). Our suppliers are fully certified, halal, kosher, fssc and USDA organic. We can also supply other coconut products, like coconut water, coconut water powder, coconut milk, coconut milk powder & more.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and desiccated coconut.

We are always looking to grow our supplier base with companies capable of delivering high quality food ingredients at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

Purchasing commitments for almonds are occurring at a slower pace compared to last year. According to the latest Almond Position Report, domestic and export commitments totaled 164 million lbs by the end of September, about 23% behind the prior year period.

Due to the uncertain trade climate, many buyers have been covering their almond needs on a hand-to-mouth basis rather than extending high volume contracts long into the future. We are seeing weaker demand from China, Turkey, the UAE, and the EU in particular. Another driver of lower shipments may be related to the early season frost, which caused many suppliers to pull off the market and only offer limited amounts while the impacts were assessed.

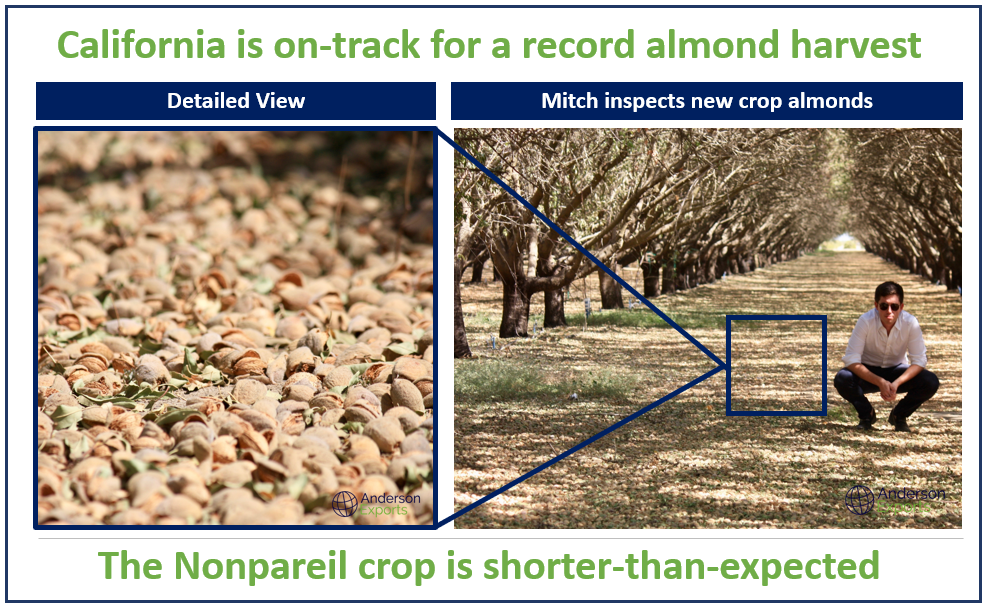

The Nonpareil crop is thought to be shorter than expected. Amid these early reports of a smaller crop, the market was sloppy for some time, with a wide spread of pricing. More recently, prices have demonstrated some stability.

Our most popular almond varieties are Nonpareil, Independence, Butte/Padre, and Carmel types with the most popular grades of Supreme, Extra, Standard 5%, and more.

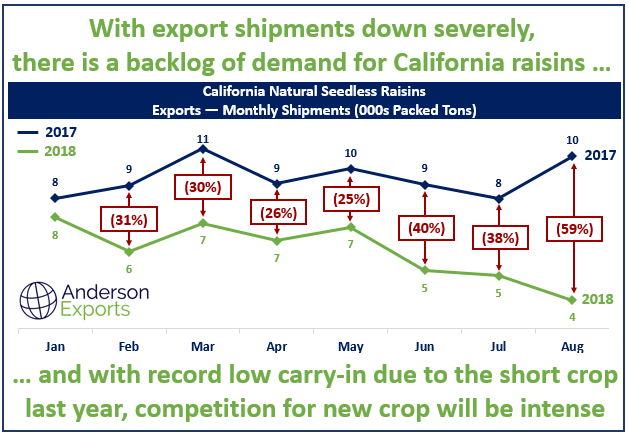

California raisin prices are stable and the new 2018 crop shipments are starting. Foreign importers are especially keen to receive the first shipments of the new California Thompson raisins. Export shipments of Natural Thompson Seedless raisins have been much lower than normal this year. The latest October figures showed export shipments down by 59% compared to the prior year, according to data from the Raisin Administrative Committee (RAC).

These shipment figures show that there may be some pent-up or “overhanging” demand, as some customers who made contracts with California packers last year did not receive the total number of containers they had contracted due to the historic shortages faced this past year in California. This means there are some buyers who will be receiving the first shipments of the 2018 crop at last year’s prices, on last year’s contracts. We see the likely primary drivers of this year’s price as consistent demand, historically low carry-in levels (approx. 70,000 MT), and the premium California’s global customer base is willing to pay for what are widely known as the world’s best raisins.

We supply all major bulk California raisins including dried-on-the-vine (DOV) and tray-dried Thompson Seedless Selects, Selma Petes, Flames, Goldens, and other varieties in Jumbo, Select, and Midget sizes and welcome your inquiries.

South Africa is almost completely sold out of the 2018 crop. New crop is expected to begin being harvested during the first quarter of 2019. South Africa has been increasing its tonnage year-over-year for some time now. We recently met with one of our large South African raisin suppliers and were informed that South Africa is estimated to produce around 70,000 MT of raisins this year. Much of this tonnage will go to Europe with another increasing portion of the crop going to to buyers in China.

Our suppliers have also reported a large number of new plantings for the Selma Pete, DOV variety of raisins. This is a similar trend seen in California’s Central Valley, as many suppliers are either transitioning older vines or planting new vineyards with the Selma Pete variety. South Africa and California are so focused on this variety because Selma Pete is reported to not only produce a sweeter raisin than a Thompson, but also a larger total volume of final product with 69% higher than average “B or Better” (B&B) numbers.

Chile is essentially sold out for their 2018 crop, with new crop expected to begin its harvest, like South Africa, in the first quarter of 2019. Many of our suppliers in Chile are reporting that they are completely sold out of dark raisins from 2018, with only some small quantities of Golden raisins still available to ship. Due to the large uncertainties surrounding the Trump Administration’s tariff wars globally, we saw many Chinese buyers and other affected markets transition from filling their needs with California raisins to Chilean product. While it may be tempting to source from Chile due to the lower prices and favorable free trade agreements, the overall quality lags behind that found in California. This is because Chilean raisins are made from grapes rejected by the table grape industry while California raisins are made from fresh grapes grown expressly to be dried into raisins.

The California walnut harvest is underway. With many early varieties almost fully in and off the trees. The season began with much apprehension from sellers, opening at some of the lowest levels seen in many years. This caused buyers to wait, and wait, and wait. Buyers staying off the market early this season brought pricing levels for in-shell walnuts down early this year as compared to previous years. Many suppliers were offering Chandler J/L under USD $1.00 / lb. CIF. We advised buyers to jump in at these historically low levels. Despite this advice, many buyers opted to continue to wait. Instead of seizing on the opportunity to book fantastic quality material at incredible pricing, many buyers thought it prudent to focus on haggling over 1 or 2 cents per lb and in fact MISSED these low prices entirely!

The most recent news from our suppliers in the Linden area, and elsewhere in California, is that the Chandler crop may be much smaller than first projected. This is causing many of the largest suppliers to hold off the market to determine how much smaller this year’s Chandler crop is before re-entering the market with what will likely be higher pricing.

The popular early varieties of Howards and Hartleys have been shipping, with reports from the orchards of higher than average meat yields for Howards, with little to no tip-shrivel. This is good news for customers who buy in-shell products from California.

The California Walnut Board’s Monthly Management Report details shipment figures for September 2018 show lower in-shell shipments than at this time last year. The weaker in-shell shipment figures for September may be evidence of buyers’ early apprehension, as outlined above. However, these weaker numbers could also be due to environmental issues, as growers are reporting that this year’s Chandler crop matured a few weeks later than previous years, which would also delay shipments in a material way.

As the newest chandler numbers become more widely available this fall, the industry will get a better idea of the total tonnage they actually have to sell. It is hard to say when California suppliers will again be offering in-shell Chandler walnuts, but when sellers do come back into the market, It is unlikely we will see in-shell pricing anywhere near the low opening levels of this season.

We work with California’s top walnut packers to supply our customers with Jumbo and Jumbo / Large (J/L) in-shell Chandler, Howard, Hartley, Vina, Tulare, Serr and other varieties. We also supply California shelled product including Chandler and non-Chandler Light Halves & Pieces (LHP) 20%, 40%, 80% and higher based on customer requirements.

Early reports suggest the new cranberry crop may not be as strong as expected earlier in the year. In Wisconsin, cranberry production is thought to be down compared to last year and in Massachusetts, there are some concerns about rot. Though the extent of impact remains to be seen, the prospect of tight supply again in the year ahead seems likely. The harvest was also a bit delayed this year--extending the period in which sweetened dried cranberries (SDCs) are hard to come by -- and, when found, come at high prices.

There will be a few more weeks until firm pricing is available widely for 2019 cranberry prices. With the 2018 cranberry crop effectively sold-out, SDCs may become more expensive in the year ahead. While prices may rise further, the increases should be more modest than the 30-40% increases observed in this past year. SDC pricing in 2019 has yet to fully take shape so we’ll have to wait and see. Given the issues with prompt availability, we continue to advise early planning and action on sweet and dried cranberry procurement and we welcome your inquiries.

Details of the Handler Withholding also indicate that the impact on SDC pricing may be somewhat mitigated since producers have the option to dispose of as much as half of the restriction in the form of concentrate, rather than SDCs. The disposed fruit must originate from the current crop year. The 15% Handler Withholding for the 2017 crop proposed by the Cranberry Marketing Committee (CMC) was approved by the USDA. However, the decision remains unknown for the 2018 Producer Allotment which would mandate a 25% disposal of cranberries. If the next Handler Withholding passes, supplies would surely tighten and firm-up prices for SDCs. Together, the potential for a weaker-than-expected new cranberry crop and the passing of the 2018 Handler Withholding are key catalysts for supply tightness and firmer prices going forward.

We supply Conventional and Organic Whole or Sweetened Dried Cranberries (SDCs) packed in bulk cases as well as 50 Brix and 65 Brix cranberry concentrate shipped in bulk 55 gallon drums.

The Pistachio harvest is underway in California with the first reports from processors describing a crop that has a smaller nut size, on average, than last year. For comparison, one of the most common sizes of California pistachios, the US Extra #1 21-25, has had its sizing range extended to account for the smaller average nut sizes seen as the crop is received from the fields. This means many pistachio sellers are currently offering their US Ex. #1 21-25 as a 21-26 or even 21-27. Pricing for pistachios will likely remain firm in the year ahead due to the very strong global demand and relatively small and highly concentrated supply.

There have been early reports of hurricane damage, although the full extent of the damage remains to be seen. The harvest is beginning in much of the southern United States, with many sellers positive about a good quality crop.

We supply Fancy Junior Mammoth Halves (FJMH), Fancy Mammoth Halves, Fancy Pieces, and other sizes / types for all major U.S. pecan varieties.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and desiccated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

California raisin prices are stable for the new 2018 crop and forward contracting is underway. Buyers are finding some relief in the relatively lower prices compared to the higher prices for last year’s short and rain-damaged crop. Foreign buyers are also eager to renew California raisin shipments to their markets. Export shipments of California Natural Seedless raisins were down 59% in August compared to the prior year, according to data from the Raisin Administrative Committee (RAC).

Weather has been favorable and quality is expected to be strong for California raisins this year, avoiding the quality issues and short supply experienced last year due to rains during the harvest. We anticipate shipment volumes to recover to normal levels in the coming months since much-anticipated new crop shipments will begin this month.

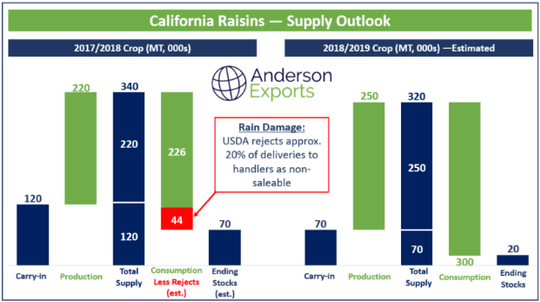

We expect the total supply of California raisins to be approximately 335K MT, consisting of ~260K MT from 2018 production and ~75K MT from 2017 carry-over.

While production recovered compared to last year, total supply is relatively unchanged due to the lower carry-in. The carry-in to 2018 is only ~75K MT, which is 44% lower than the 5-year average carry-in for California Natural Seedless Select raisins. As much as 50K MT of the industry carry-over may be held by Sun-Maid and destined for retail, not bulk raisin export markets. Planted raisin acreage is also in a state of steady decline due to raisin vine pull-outs as farmers plant walnuts, almonds, and other crops.

We have seen exceptional quality from California’s new raisin crop as early loads come in from the fields. In 2019, we expect Asia to continue to displace Europe as the world’s largest export market and Japan to be the largest importing country. Asia has a growing middle-class consumer base which has increasingly more access to, and ability to pay for, imported California raisins. Increasing penetration of e-grocers will not only educate consumers about California raisins, but also introduce California raisins to ever larger consumer audiences in Asia. We have seen our strongest demand for California raisins from our own customers in Japan, China, Taiwan, South Korea, Singapore, Thailand, and the Philippines.

We supply all major bulk California raisins including dried-on-the-vine (DOV) and tray-dried Thompson Seedless Selects, Selma Petes, Flames, Goldens, and other varieties in Jumbo, Select, and Midget sizes.

Amid weaker prices and record global supply, California walnut handlers face a challenging year ahead. The graphic below illustrates the growing production and acreage of the California walnut industry, based on data from the USDA.

Walnut acreage in California and in other regions is on the rise. California anticipates a crop of 690K Short Tons, which is an all-time record. Chile will have carry-in for the first time ever. China also continues to grow a massive crop in the range of 800K MT, which is consumed domestically. Growth in the supply of walnuts is increasing due to production increases in California, China, Chile, and in the Baltics.

Contracting volume early this year is especially important for California’s in-shell-only packers since they do not have the ability to crack their walnuts themselves. In-shell-only packers who miss the inshell selling season this year because they “want to hold off the market and wait for prices to come up” or “protect their brand” will find themselves in a dire situation if prices remain weak.

There is a silver lining here: an extended period of lower prices and growing supply may build up new destination markets for California walnuts. As prices come down, previously inaccessible markets will be opened and new consumers will be introduced to California walnuts as a delicious and nutritious ingredient. Introducing new consumers to California walnuts will in turn increase the overall demand. Increasing overall demand will ultimately help to rebalance the oversupply and buoy prices.

All varieties are coming in slightly later than expected this harvest season. Some growers and packers are seeing a slight increase in edible yield due to a general lack of tip-shrivel. Howard, Hartley, and other early varieties are being received now, with the expectation that first receipts of Chandler will begin to come in off the trees this week or next.

Please let us know if you have a current need, or would like to book forward contracts for, Jumbo and Jumbo / Large (J/L) inshell Chandler, Howard, Hartley, Vina, Tulare, Serr or any other California walnut varieties. Many customers have also booked contracts for Chandler and Non-Chandler LHP 20%, 40%, 80%+, and more. We can also provide Bleaching for inshell products and vacuum-packing or nitrogen pillow-packing for shelled products.

In preparation for the 2018 cranberry harvest season we visited Wisconsin, the largest production region of cranberries in the U.S. The weather has been favorable and the crop is coming along nicely. With cool evening temperatures and warm humid days this summer, our Wisconsin growers are reporting excellent sugar maturation leading up to this year’s harvest.

Supply remains tight due to shortages of sweetened dried cranberries (SDCs) due to last year’s small cranberry crops in the U.S. and Canada. Lead times remain long and material for prompt shipment is increasingly hard to find with most packers holding off the market or offering at premium prices for forward shipment, if at all. The industry still awaits the USDA’s volume regulation decision, which may further constrain supply. Some packers will have periodic availability for prompt shipment although most will only be booking for shipment in 2019.

Our visits to Wisconsin cranberry bogs and the processing facilities for whole and sliced SDCs can be seen in the graphic below. During this trip, we gained further insight into the mechanics of SDC production. We highlight below the key methods and processes involved in bringing you the world’s best quality sweetened dried cranberries.

The cranberry harvest occurs in the late fall months, after which cranberries are frozen prior to processing into the first SDCs available for shipment in December 2018 or January 2019, depending on the packer.

New crop cranberry shipments, unlike almost every other dried fruit or nut product, DO NOT begin promptly after the receipt of the new crop cranberry harvest. In fact, once harvested, cranberries are first put into cold storage where they are left to freeze solid over several months. The freezing process prepares the fruit for eventual SDC production. All freshly manufactured SDCs are made from fruit that has been frozen for at least several months. “New Crop” for SDCs is therefore somewhat of a misnomer as all SDC products are processed exclusively from frozen fruit and this freezing process takes many months. Once a new lot of SDCs is produced, the product typically has a stable shelf-life of 24 months.

Please let us know if you have a current need, or would like to book forward contracts for, Organic or Conventional Whole or Sliced Sweetened Dried Cranberries (SDCs). We also supply 50 Brix and 65 Brix cranberry concentrate, shipped in bulk 55 gallon drums.

The almond market is on hold as the talk of California type varieties coming in short continues. Suppliers are also awaiting the position report which will come out next week.

All major California Almond varieties will be available to ship in the coming weeks as many buyers are beginning to book their forward inventories. Our most popular almond varieties are Nonpareil, Independence, Butte/Padre, and Carmel types with the most popular grades of Supreme, Extra, Standard 5%, and more.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and desiccated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

We visited multiple raisin processors in the Central Valley of California this week to discuss the new crop and forward pricing for the 2018 California raisin crop.

The vines are no longer resting this year and weather has been favorable so bunch counts are up significantly compared to the prior year. In one raisin plot in Kerman, California we learned that bunch counts recovered to 34 bunches per vine this year compared to 18 bunches per vine in the prior year, up 89%. Consistent with improved bunch counts and yields, we also observed substantial increases in the number of trays per row compared to last year, which is of course another positive indicator for the new crop. There is no rain or adverse weather in the 15-day forecast so the quality of the new raisin crop should be exceptional.

Despite the rebound in production, total supply will be relatively unchanged compared to last year due to the record low carry-in. For 2018, we expect total supply of approximately 335K MT, consisting of ~260K MT from 2018 production and ~75K from 2017 carry-over. The total supply for bulk raisins is probably even lower since as much as ~50K MT of the industry carry-over may be held by Sun-Maid and destined for retail, not bulk raisin export markets.

Pricing for 2018 crop bulk California raisins is opening at reasonable levels. Customers buying at expensive prices for 2017 crop over the past few months are finding some relief in the lower prices for the new 2018 raisin crop. Opening prices are generating new contracting momentum and also leaving room for steady price increases throughout the season, which is ideal for processors and foreign importers. Demand for new crop from foreign markets in Asia should be particularly strong as shipment numbers from California have been significantly below normal in recent months. Shipments of California Natural Seedless raisins to export markets totaled only 4,192MT in August 2018, 59% lower than the prior year period. We anticipate stable and slowly rising prices for bulk California Thompson raisins.

California’s new crop raisins are of excellent quality and as the harvest gets underway, we believe it is important to inform our buyers of California’s key raisin products and their differences. The graphic below shows the primary attributes of California’s two most commonly exported raisins: Thompson Seedless (Tray-Dried) and Dried-on-the-Vine (DOV). It is important to note that the distinction of DOV specifically describes the drying / harvest process, not a difference in variety as a single variety of grape can be either tray-dried (Thompson Seedless) or Dried-on-the-Vine (Thompson DOV).

As California comes to market with extremely high quality fruit, Turkey is grappling with unprecedented currency volatility. In this unknown environment, forward contracting in Turkey with high confidence is all but impossible. Based on the extent of recent swings in the Lira, currency movements of a single day can ruin an otherwise profitable raisin contract from Turkey. The extent to which this instability will incentivize Turkish raisin buyers to reconsider their supply sources remains to be seen. To be sure, price motivations have clearly dominated many European buyers’ shift to Turkey but if currency issues persist or quality problems arise, some buyers may reconsider.

We are pleased to present the following product showcase for Selma Pete DOV Double-Run Supreme raisins.

We supply all major bulk California raisins including dried-on-the-vine (DOV) and tray-dried Thompson Seedless Selects, Selma Petes, Flames, Goldens, and other varieties in Jumbo, Select, and Midget sizes.

The California walnut new crop is developing well. The weather has been ideal with the harvest underway for the early varieties of Vina, Serr, Howard, and Hartley. California packers are receiving a smaller than usual number of forward contracts vs this time last year. Opening prices are low with processors aware that it is a buyers market right now. Processors also know that seasonal demand from Europe and the Middle East are not yet fully expressed in the market price. Some processors may be keen to get forward business on the books at the current low prices while other larger processors are not anxious to undersell what is shaping up to be an excellent crop.

Chandler inshell will be available to ship in the first half of October. Early varieties such as Vina, Serr, and Hartley are already being received by California walnut processors. Jumbo and Jumbo / Large Hartley Bleached, Jumbo Howard, Jumbo Chandler, and Jumbo Large Chandler available for booking.

Prices remain high for sweetened dried cranberries (SDCs) as supply remains tight. With extremely limited near-term availability, there is no spot market for prompt shipment from origin. Though the new crop is developing well, anxiety still surrounds the possibility of the USDA’s approving a 25% volume reduction across the U.S. cranberry industry. We supply organic and non-organic whole and sliced sweetened dried cranberries (SDCs) from Wisconsin, Massachusetts, and Canada.

California Almonds are on track to hit a record breaking crop for the 2018 harvest. Early indications suggest that the nonpareil crop may be short. Our recent visit to California’s Central Valley reaffirmed reports that this almond crop is of very high quality as the first field-run product is received by processors for packing.

All major California Almond varieties will be available to ship in the coming weeks as many buyers are beginning to book their forward inventories. Our most popular almond varieties are Nonpareil, Independence, Butte/Padre, & Carmel types with the most popular grades of Supreme, Extra, Standard 5%, and more.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and desiccated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

According to a report by Daniel Sumner and Tristian Hanon from UC Davis published in August 2018, the share of pecans shipped to countries with retaliatory tariffs on the U.S. (~22%) is higher than the share of walnuts (~14%), almonds (~13%), and pistachios (~13%) shipped to markets facing increased tariffs.

The report, which assesses U.S. fruits and nuts found that the trade losses may total to $2.64 billion per year using the export value lost as a measure.

Our earliest new crop shipments are for late September / early October. We supply Fancy Junior Mammoth Halves (FJMH), Fancy Pieces, and other sizes / types for all major U.S. pecan varieties.

The U.S. pistachio crop is developing well. Expect new crop shipments in October and November. We supply all major grades and sizes of in-shell and kernel Pistachios from the U.S. and welcome your inquiries for new crop.

California walnut production is estimated at 690K MT, up 10% from the crop of 630K MT last year according to the 2018 California Walnut Objective Measure Report released by the USDA.

The data indicated an average nut set of 1,176 per tree, up 3.1% from the 2017 average of 1,141. Sizing data came in small -- all of the sizing measurements were below the prior year levels. Although there were some concerns that rains in the late spring would damper the crop, it turned out to the contrary: cooler conditions increased kernel size and improved quality. All told, California is on track for a good walnut harvest which will kick-off in the middle of this month.

For those buyers who are looking for the best potential for high quality inshell, we recommend sourcing your product from the world renowned Linden area, which grows some of the highest quality and most sought after nuts in California. Up and coming regions with increasingly higher quality production also include the Northern areas of Chico and Yuba City. The rise of these growing regions is in no small part due to the climatic changes caused by the increasing pressures of warmer average temperatures seen over the past decade in California’s Central Valley. These higher temperatures create risk of sunburn, infestation, and issues of water availability. Fortunately for California’s walnut industry, Northern California has reliable water resources and a more mild climate, ideal for growing these incredibly healthy nuts.

The cranberry harvest is now only a few weeks away. The 2018 cranberry crop is expected to be normal which will likely register as a year-over-year increase compared to 2017 when production was down in the U.S. and Canada. While production is expected to recover, total supply for 2018 / 2019 will be similar to this past year due to lower carry-in and the USDA volume regulations. The potential for the 2018 handler withholding to pass provides further runway for higher prices for sweetened dried cranberries (SDCs). The Cranberry Marketing Committee meeting in mid-August provided further clarity on the handler withholdings (supply reductions).

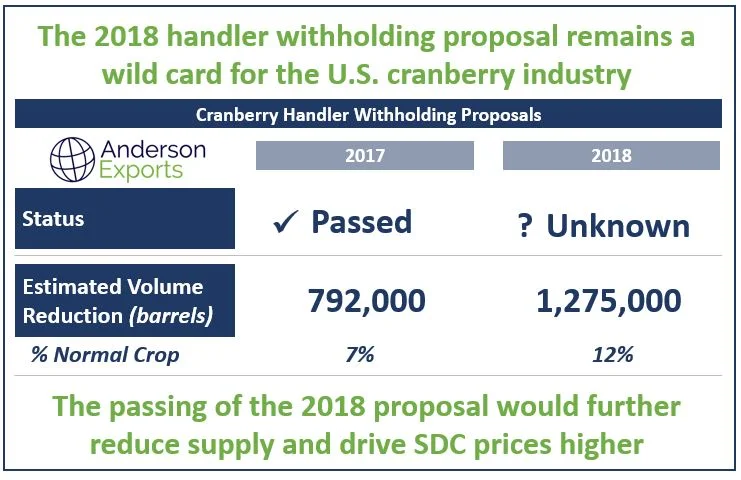

The USDA ruling which approved the Cranberry Marketing Committee recommendation to impose a 15% handler withholding on the 2017 crop is being enforced. In total, an estimated 792,000 barrels of cranberries will be removed from U.S. inventories as a result of that ruling, which is about a 7% reduction versus a normal harvest. Since the 2017 crop was down due to natural causes, this artificial supply reduction compounded supply tightness. Amid strong global demand for SDCs, prices have doubled compared to a year ago and show no signs of reversing in the foreseeable future.

The 2018 handler withholding remains a wild card for the cranberry industry. The USDA has still not released the final ruling and producers are frustrated as the consequences of this decision are far-reaching. At the Cranberry Marketing Committee meeting in August, the guidance from the USDA was to proceed with the assumption that the USDA will publish a final ruling consistent with the proposal issued in April. Based on that proposal, it is estimated that the 2018 handler withholding will remove 1,275,000 barrels of cranberries from U.S. inventories, which is about a 12% reduction versus a normal harvest. Given that the market is already extremely tight, the passing of the proposed handler withholding for 2018 would likely give prices further upward momentum.

For buyers with uncovered SDC needs for the fourth quarter 2018, we have some limited availability and would advise reaching out before the production slots are filled up. Given how much prices have come up in the last year, many customers have responded by covering on a hand-to-mouth basis with single loads here and there. This tendency to buy spot instead of through forward contracts may prove to be a costly strategy if forward material is not contracted and the 2018 producer allotment passes. We supply sliced and whole sweetened dried cranberries from Canada and the U.S. and welcome your inquiries.

Yesterday the Raisin Bargaining Association sent out a letter stating the field price offer to packers for the 2018-19 raisin crop. The price offered is the highest in the history of California Raisins and reflects the very low inventory position and the reduced acreage producing raisins. The inventory as of August 1, 2018 was approximately 79,000 tons. This is a reduction of over 40,000 tons from August 1, 2017. Based on this, the growers would need to produce 40,000 more tons than they produced in 2017 just to have the same available tonnage. Weather conditions during the harvest have been exceptional and most in the industry are very optimistic that the crop will be of excellent quality.

With the 2018 California raisin harvest underway, buyers are eager to lock-in new crop contracts. California raisins are known for being the highest quality in the world due to experienced farmers, ideal growing conditions, advanced processing equipment. Natural Thompson Seedless Select raisins are the most sought after raisin variety and size. With shipments of California Thompson raisins down substantially compared to last year, buyers have been covering with other regions -- namely, Turkey, Chile, and South Africa. When the new crop becomes available in the coming weeks, we expect monthly shipment numbers to rebound. Prices will likely remain firm even if the new crop is normal due to extremely low carry-in. From California, we supply Thompson Seedless, Selma Pete, Fiesta, Zante Currant, Flames, Golden Seedless in Jumbo, Select, and Midget sizes and welcome your inquiries.

The new nonpareil crop is rolling in and early reports suggest that sizing is a little small. Of course, these are preliminary reports so the extent of the issue remains to be seen. Nonetheless, this week, many almond suppliers were off the market or only offering “safe” pricing way above the current market. With tariff uncertainty compelling many buyers to stay on the sidelines, forward contracting activity is lagging prior years. However, global demand for almonds is robust and we expect the market to pick-up soon as new crop shipments become available.

Trump’s trade war is having mixed impacts on the California pistachio industry. On the positive side, sanctions on California’s key pistachio growing rival -- Iran -- will likely allow California to take market share in the global market. On the negative side, major buyers of Pistachios are in countries such as China which are being targeted by Trump’s tariffs. As a result, retaliatory tariffs on pistachio imports from China will dampen California’s ability to serve key export markets. With the new crop on the way, the impacts remain to be seen.

The incentives for Brazilian mills to produce sugar sweetener compared to ethanol is extremely low right now. Therefore, much of the cane typically destined for sugar is being diverted to ethanol. These trends are weighing on estimates for how much sugar will be exported by Brazil in the years to come. All told, even with the diversions to ethanol, Brazil is a key global bulk exporter of sugar and that role will likely remain unchanged. Particularly on vessel-load business, other countries have a hard time competing with Brazil due to the favorable cane growing conditions in the country and the sophistication and scale of the industry.

We supply Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 12,500 MT) or forward contract basis including long-term contracts of 300,000 MT / month x 12 months. Payment by SBLC, BG, or DLC confirmed by global top 50 bank. We supply German Beet Sugar (MOQ: 1 FCL) as well as Thai Sugar (MOQ: 10 FCLs)

Next month, soybean planting will begin full-throttle in central Brazil. Particularly due to Chinese tariffs on U.S. agricultural products such as soybeans, Brazil is in a relatively advantaged position vis-a-vis the U.S. Planted soybean acreage is on the rise and Brazil and the country is expected to continue in its role as a key global supplier of soybeans in the years to come.

We supply GMO and Non-GMO certified Soybeans from Brazil. MOQ: 12,500+ MT. Payment by SBLC, BG, or DLC confirmed by global top 50 bank.

Full-season corn is typically planted this month in Brazil. Corn is predominantly grown in the Southern and Southeastern regions of Brazil. During this month, scattered rains are expected and warm to hot temperatures.

We supply GMO and Non-GMO certified Corn from Brazil. MOQ: 12,500 MT. Payment by SBLC, BG, or DLC from global top 50 bank.

We offer a wide range of rices from Thailand and Cambodia including Gaba Jasmine, Thai Fragrant, Thai Hommali, Thai Black, Thai White, Thai Red and Thai Parboiled Rices. MOQ: 10 x 20’ FCLs.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and desiccated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

California raisins are about 3 weeks from harvest. The 2018 California raisin crop is healthy and developing well so far. Bunch counts recovered compared to the prior crop. The Raisin Bargaining Association (RBA) reported 33 bunches per vine for the current crop, up 22% from last year but still below the 10-year average of 37 bunches per vine. Weather, as we saw last year with the two unexpected rains during the harvest, is of course a key factor for a successful raisin harvest and will be especially in focus in the coming weeks.

Prices for bulk California raisins will likely remain elevated even if the new crop is normal. The current raisin crop was the smallest since 1982 according to the RBA. Due to the record small crop this year, the carry-in for 2018 supply is estimated to be ~70 - 75K MT, or ~48% lower than the 5-year average. Demand for California raisins has built-up considerably in recent months as monthly shipment numbers lag severely behind recent years. Shipments of California Natural Seedless raisins were down by 41% in July compared to the prior year based on the latest report from the Raisin Administrative Committee (RAC).

California raisin suppliers are therefore eager to renew supply continuity for both domestic and international clients. Buyers are similarly looking forward to new crop, particularly for Select / Medium sizes of Thompson Seedless raisins which can be hard to come by at this point in the year. Midget / small sizes, which fall through the screens first compared to larger fruit, are available from the current crop at attractive levels.

After last year’s disappointing raisin crop in California, major importers turned to Turkey, Chile, and South Africa to cover supply in recent months. California processors even imported Chilean material to fulfill domestic customer needs. Chilean raisin exports to the United States increased by 54% from January - May of this year compared to last according to data from the USDA. While the swing is notable, Chile’s total raisin production of ~60K MT still lags the United States and Turkey by a substantial margin. For example, in a typical year, California ships ~20K MT of raisins per month so it would take only 3 months to ship Chile’s entire annual production volume. Nonetheless, quality from Chile this year has been excellent and we have loads available for prompt shipment from Chile for Thompson and Flame raisins.

Turkey’s new crop for raisins is also just around the corner. With the Eid al-Adha holidays ongoing, the market in Turkey will be slow for the next week. Turkey’s Minister of Agriculture, Mr. Pakdemirli recently announced the new crop estimate for Turkey at 261K MT. The actual figures often differ substantially from the government’s estimates so we will have to wait and see. Turkish Sultana raisins and Thompson raisins will be first shipped to Spain, due to its close geographic proximity, then to Europe and other export markets. Though Turkey has continued to grapple with observing strict pesticide controls, overall, the quality of Turkey’s raisin processing facilities is improving. For Turkish raisins, we supply from BRC and ISO 22000 suppliers to deliver the highest quality Turkish sultana raisins to our customers.

Trump’s recent spat with Erdoğan is causing major problems and concerns for Turkey’s trading partners. We have seen large fluctuations in the value of the Turkish Lira, which will certainly affect the rates at which raisins are offered to Turkey’s foreign purchasers. Due to the general uncertainty around the Lira, we have seen many Turkish suppliers reluctant to offer large forward contracts.

Iranian sultana raisin exports outside of the Middle East will face major challenges in the coming year due to the U.S. sanctions. Trump intends to clamp down on businesses and banks doing business with Iran. European buyers of raisins from Iran will likely turn to Turkey, Afghanistan, Uzbekistan, the U.S., Chile and South Africa this year due to these trade and sanction issues.

We specialize in sourcing the highest quality sun-dried raisins from California, Turkey, Chile, and South Africa and we we welcome your inquiries for dried-on-the-vine (DOV) and tray-dried Thompson Seedless, Selma Petes, Flames, Goldens, and other varieties in Jumbo, Select, and Midget sizes. Currently, we also have Chilean and South African raisins for prompt shipment.

Severe fruit shortages of sliced sweetened dried cranberries (SDCs) continued in recent weeks. Producers have no availability for prompt shipment. Lead-times to earliest shipment remain long and prices are high and have shown no weakness yet. The USDA decision on the 25% producer allotment (supply reduction) for the coming crop still remains unknown at this time. Given the substantial impact this decision will have on the industry and fruit availability, the tightness in pricing and supply may become even more problematic if the supply reduction is passed.

For buyers, the current situation is no doubt challenging. Prices have doubled over the last year and show no signs of relenting at this time. There is no longer a spot market for prompt shipment due to the shortages. The U.S. is also essentially the sole supplier of cranberries around the globe, besides a very small crop from Chile, so there are no actionable alternative supply origins for sourcing cranberries. Therefore, we urge our clients to discuss their cranberry requirements with us as early as possible in order to determine the right approach to covering forward needs for SDCs.

The new walnut crop in California is looking good. Some walnut growers have been doing some cuttings in recent weeks and have reported that the color of the walnuts is better than at the same time last year, which is a positive sign. The Objective Walnut Estimate is set to be released in September by the California Agricultural Statistics Service (CASS) and should add further clarity on the size of the 2018 California walnut crop. Current estimates are in the 680 - 700K MT range.

Export sales have been slow in recent weeks due to the tariffs. Currency volatility is also adding to buyer reluctancy to book forward contracts. The market may pick-up after the details of the Section 32 buys are released. This is the relief channel for the walnut industry on the trade war. We expect market activity to pick-up in the coming weeks.

The Walnut Acreage Report for California released in July 2018 showed 335,000 bearing acres for California, a new record which positions the industry well for a record crop. The 2017 bearing acreage is composed primarily of Chandler (47%) followed by Hartley (12%), Howard (11%), Tulare (11%), Serr (5%), Vina (5%), and others (10%). There are also approximately 65,000 non-bearing acres for the 2017 year, according to the USDA. Chandler represents the 59% of the non-bearing acreage. These trees will begin to produce in the coming years, adding to the bearing acreage and total production.

California has the lightest and largest walnuts in the world. We supply in-shell and shelled walnuts for all major varieties including Chandler, Hartley, Howard, Tulare, Serr, Vina, and others.

Foreign buyers continue to be cautious with forward contracts for the new crop. However, current-year almond shipments are still going strong through the typical transshipment routes into China via Vietnam, Hong Kong, etc. The July 2018 California almond shipment report showed July shipments at 143 mm lbs, down slightly from the prior year figure of 153.9 mm lbs. The lower committed shipments of 170 mm lbs, down 15.65% confirms the slow forward contracting environment. Global uncertainty on tariffs, foreign exchange volatility and a large crop may keep put a lid on pricing this year for some California almond varieties.

We anticipate almond prices to be steady. Cals are harder to come by at the moment. The Cal SSR crop is coming in a little short vs. last year. Growers and processors are expecting approx. 285 mm of SSR grade product this year. Supply is not keeping up with demand on SSRs so expecting firmer pricing there.

The new California walnut crop quality looks good, although we still have another six weeks of summer weather to get through before we’re safe. In a hot year like this, well-irrigated orchards will perform particularly well. Georgia’s crop is looking especially strong with estimates in the 110 - 140 million lbs range. Estimates for the U.S. and Mexico pecan crops are in the 300 mm lbs and 330 mm range, respectively.

Our earliest new crop shipments are for late September / early October. We supply Fancy Junior Mammoth Halves (FJMH), Fancy Pieces, and other sizes / types for all major U.S. pecan varieties.

Trump’s resumption of sanctions on Iran is positioning U.S. pistachio suppliers for big share gains. Iran is the only real rival to U.S. pistachios in terms of production volume followed by Turkey. The estimated carry-over to new crop is going to be smaller than in typical years which may drive firmer opening prices. As we approach the harvest season, focus will be on weather and trade tariffs.

The U.S. pistachio crop is developing well. Expect new crop shipments in October and November. We supply all major grades and sizes of in-shell and kernel Pistachios from the U.S. and welcome your inquiries for new crop.

Turkish Figs have seen a recent rain while the product is in its most critical stage for harvesting. We have heard reports that up to 40% of figs will be either sour, open-mouthed, or cracked. We have seen this movie before this past year in California raisins. These types of late season rains during critical junctures in the process of harvesting creates major problems that stem from the damage these rains can do. This past year in California, as we have talked about extensively, has shown the monthly shipments to be down some 40+ percent in July vs. this time last year.

This is a big deal for Turkish Figs as it will bring two-fold results to this large export market; 1) We will likely see a large decrease in total available tonnage in the coming year (2018 / 2019) vs last year due to mold, sand, and grit concerns and 2) The price of Turkish Figs will thus begin to climb beginning now through this coming year. We saw the same in California raisins last year, with many buyers holding off the market during the early fall harvest season, when prices were at their lowest they would be all year. This has caused a backlog of orders with lower quality and higher prices. We ultimately recommend that anyone interested in booking their Turkish Fig needs for this season books this business sooner rather than later to avoid the inevitable rises in price and lower quality to be expected from Turkey after the recent rains.

The Turkish dried apricot harvest is nearing an end. The quality of the crop is good. The average sizes are in the 3 - 4 range. The estimated carry-in to the 2018 crop is about 30K MT. Organic and non-organic sulfured and unsulfured Turkish apricots are available for export markets in size 3, 4, and 5.

Sugar prices remained low in recent weeks as world market surpluses continued. Large production increases from India and Thailand added to the excess supply situation. After production quotas expired in October 2017, the E.U. sugar industry is facing an extremely challenging export environment given the low price environment. Recent droughts in the E.U. are weighing on production estimates as well.

We supply Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 12,500 MT) or forward contract basis including long-term contracts of 300,000 MT / month x 12 months. Payment by SBLC, BG, or DLC confirmed by global top 50 bank.

We supply German Beet Sugar (MOQ: 1 FCL) as well as Thai Sugar (MOQ: 10 FCLs)

Brazil’s exports of soybeans are expected to hit an all-time record this year. The 25% Chinese tariff on U.S. soybeans is set to improve Brazil’s relative competitiveness compared to the U.S. In the first half of 2018, Brazil’s exports of soybeans to China increased to approximately 36 million metric tons, up about 6% from the prior year. In July alone, Brazilian soy exports to China rose 46% compared to July last year.

Weak sugar prices are also incentivizing Brazilian farmers to switch from sugar to soy and other crops. According to government data, Brazil’s soy plantings grew by 2 million hectares in two years while, over the same period, planted acreage for cane sugar declined by 400,000 hectares.

We supply GMO and Non-GMO certified Soybeans from Brazil. MOQ: 12,500+ MT. Payment by SBLC, BG, or DLC confirmed by global top 50 bank.

Estimates for Brazil’s 2017 / 2018 corn crop declined slightly in recent weeks to 82.1 million tons (MMT) which reflects a decrease of 16% compared to last year’s production of approx. 99 MMT. Brazil’s corn exporters continue to be well-positioned to take advantage of Trump’s trade disputes with key trading partners.

We supply GMO and Non-GMO certified Corn from Brazil. MOQ: 12,500 MT. Payment by SBLC, BG, or DLC from global top 50 bank.

We offer a wide range of rices from Thailand and Cambodia including Gaba Jasmine, Thai Fragrant, Thai Hommali, Thai Black, Thai White, Thai Red and Thai Parboiled Rices. MOQ: 10 x 20’ FCLs.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. We are experts in sourcing bulk food ingredients and welcome the opportunity to work with you on your inquiries. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pine nuts, pecans, brazil nuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried black currants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and dessicated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

The new crop of California raisins is developing well with improved bunch counts compared to last year and overall crop quality is looking good. At this time, we are signing up new crop contracts for earliest shipment in September and October.

Even with expectations of a normal new crop for California raisins, we anticipate elevated prices due to the smaller carry-in and backlog of demand. Since the prior crop was so small, the carry-out from this season is probably going to be approx. 70 - 75k MT for California Natural Seedless Select raisins.

We believe this decreased carry-in figure together with the shipment backlog -- seen in the June shipments down 39% year-over-year -- will lead to tight supply and firm prices for new crop despite normal production levels.

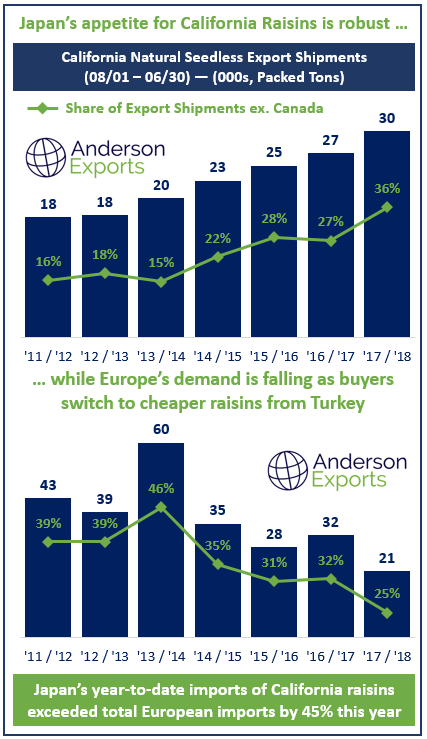

On the demand side, there is strong appetite for California raisins from Asia, particularly in Japan. Based on monthly shipment data from the Raisin Administrative Committee (RAC), the following graphic helps illustrate the shifting export demand for California raisins.

For the first time ever, Japan imported more California raisins than all of Europe over the period of August 1st to June 30th this year. Not only did Japan surpass European imports, it did so by a vast margin: 9,315 MT or 45%. We expect this robust demand from Japan to continue. Japan’s quality specifications are some of the strictest in the world and California’s processing facilities are the most sophisticated so the two regions are well-suited.

Over the last few years, Europe has become a less significant buyer of California raisins, opting increasingly for Turkish sultana raisins rather than California Thompsons, largely due to the price differential. Turkey’s proximity to Europe as well as improving processing capabilities are also driving the origin-shift.

The California Thompson is widely considered to be the best snacking raisin globally and will likely remain so for some time. We expect California raisin prices to remain elevated and buyers to act early to secure new crop material and welcome your inquiries for dried-on-the-vine (DOV) and tray-dried California Thompson Seedless, Selma Petes, Flames, Goldens, and others in Jumbo, Select, and Midget sizes.

The USDA decision on the 25% producer allotment (supply reduction) for the coming crop is long overdue at this time. They indicated the decision would be put out in Feb/March but has yet to be released. Growers need to make operating decisions with the information about the crop allotment since the implications will be severe. Availability remains tight with no prompt shipment available. Some suppliers are completely sold out of fruit and are awaiting new crop. At this time, the new crop looks okay -- doesn't appear to be the biggest crop but should be normal. Bottom line is that the USDA holds the cards on forward cranberry pricing due to the potential for the USDA to pass a 25% supply reduction for the coming crop. This decision has the potential to drive prices higher substantially.

With the earliest shipments being offered right now for September / October, and some suppliers offering January forward shipments well over $2.00 / lb. on an ex-works basis, our recommendation if you need to cover your cranberry needs prior to 2019, is to lock in contracts at today's prices.

Buyer apprehension due to uncertainty over trade tariffs is causing slower new crop sales for California walnuts. Prices have come down in recent weeks for current and new crop. Walnut handlers in California are looking to reduce inventories and accelerate new crop sales so prices are coming down. The new crop is expected to be healthy with tonnage in the 680,000 MT range. Though tariff-related uncertainty may persist for some time, we do expect order activity to pick up after the Objective Walnut Estimate is released later this month. The California Agricultural Statistics Service (CASS) Objective Estimate will add some clarity on the new crop.

Howard, Hartley, Bleached Hartley, Tulare, Vina, and Serr varieties of inshell walnut will be harvested first, with Chandler quick to follow. We are currently marketing new crop inshell Jumbo and Jumbo / Large Chandler Walnuts, please let us know your requirements.

Almond prices are declining due to the tariffs effect of weakening demand. China's tariff added a 50% tax to California almonds. Prices have come down approx 10% recently due to the bumper crop expected amid lower demand due to escalating trade tensions. As another setback for U.S. almond growers, China has closed a trading loophole that for years allowed large volumes of American almonds to be transported into the country via Vietnam without incurring import taxes. China's strict treatment of smuggling is also discouraging transshipment activity to avoid tariffs.

Overall, we see committed shipments currently down >50% from this time last year as an early signal of prices dropping substantially in the period ahead due to the bumper crop amid eroding export demand due to tariffs.

Turkish apricot shipments for the 2018 crop are underway and quality is good. Organic and non-organic sulfured and unsulfured Turkish apricots are available in size 3, 4 and 5 are freshly processed and packed. With production for the 2017 / 2018 harvest estimated in the 140,000 MT range, Turkey is by far the largest producer of apricots globally followed by Iran (32,000 MT) and Uzbekistan (10,000 MT).

Weak sugar prices continued in recent weeks as world market surpluses rose further. Earlier this year, record production from India and Thailand worsened the oversupply situation. Production in the E.U. is also growing after production quotas expired in October 2017. The E.U. faces an extremely competitive export market with global production so high and prices so low. In recent weeks, heavy rains in the Center / South Brazil slowed the sugarcane crush. Wetter weather is known to negatively impact cane quality and incentivizes ethanol production since juice quality deteriorates.

We supply Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 50,000 MT) or forward contract basis including long-term contracts of 300,000 MT / month x 12 months. Payment by SBLC, BG, or DLC from global top 50 bank.

As Trump escalates the trade war with China, Brazil and Argentinian soy farmers are seizing the opportunity to increase production. The USDA raised its 2018 / 2019 Brazilian production forecast to a record 120.5 MMT driven by higher planted soybean acreage.

Higher freight rates in Brazil are continuing to negatively impact Brazil’s soybean industry. Due to higher inland freight costs as a result of the labor disputes, fertilizer deliveries to Brazilian soybean growers have been delayed. Some growers have reported a rise in fertilizer and pesticide costs of 20% ahead of the 2018 / 2019 crop cycle. Higher fertilize prices will weaken grower margins and may lead to lower fertilizer application rates. In turn, reduced fertilizer and pesticide application rates may depress yields in the years to come. Despite near-term challenges, global demand is growing for soybeans and Brazil is extremely well positioned to serve increasing global demand.

We supply GMO and Non-GMO certified Soybeans from Brazil. MOQ: 50,000+ MT. Payment by SBLC, BG, or DLC from global top 50 bank.

Expectations for Brazil’s safrinha corn production fell in recent weeks. Many believe the lower production figures will be reflected in lower volumes of Brazilian corn exports. Reduced production is causing prices to go higher. Estimates for Brazilian production are in the 80 MMT range. Globally, corn inventories are falling faster than expected which is also firming prices. The global stocks to uses ratio is in the 13% range which is the lowest level in recent years.

We supply GMO and Non-GMO certified Corn from Brazil. MOQ: 50,000 MT. Payment by SBLC, BG, or DLC from global top 50 bank.

We work with a number of other products so please reach out if you have an inquiry for something you do not see here. Some of our other product offerings include sunflower seeds, lentils, green peas, freeze dried fruits, popcorn, dried cherries, dried apples, dried blueberries, cherry concentrate, quinoa, dried honey dates, dried cherry tomatoes, dried gojis, dried kiwis, dried strawberries, chickpeas, chia seeds, dried mulberries, almonds, macadamias, pistachios, walnuts, cashews, pinenuts, pecans, brazilnuts, pumpkin seed kernels, melon kernels, hazelnuts, dried prunes, golden raisins, sultanas, dried apricots, sweet apricot kernels, dried blackcurrants, dried figs, dried dates, popcorns, maraschino cherries, dried tomatoes, strawberry pie filling, blueberry pie filling, cherry pie filling, dried mangoes, dried gingers, dried pineapple, and dessicated coconut.

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

The biggest news leading up to this year's harvest is of course the widespread sentiment of uncertainty surrounding global tariffs and the Trump Administration's trade wars. Buyers have been hesitant to book new crop walnut shipments due to the anxiety surrounding these global tariffs moving into this year’s harvest. This will be a repetitive motif this year across all of California’s agricultural products. China has been a much publicized case of retaliatory tariffs, with many other nations moving to impose similar measures in response to Trump’s hardline trade positions. Recently, India has joined the growing list of countries specifically targeting the California Agricultural industry, announcing tariffs of 120% on California walnuts.

India imported approximately 8% of California’s in-shell crop for the 2017 / 2018 year, according to data from the California Walnut Board, which will cause a meaningful impact on trade flows. Uncertain trade relations and tariffs are already causing a remarkably slow start to new crop sales. Many suppliers we work with are reporting a fraction of the forward sales seen at this time vs. in previous years. How these trade uncertainties are affecting, and how they ultimately will affect, exports in the agriculture sector in California is hard to know at this point in the season, but the evidence so far is showing there may be few winners.

Turkey, typically California’s largest in-shell trading partner in past years, reported an 18,000 MT decrease in imports for the 2017 / 2018 vs. 2016 / 2017 crop years. Chile and China also continue to grow their output, with estimates for Chile’s production around 150,000 MT and estimates for China’s production approaching 800,000 MT.

With that said, California’s new crop for walnuts is likely to be quite large, with expectations of total crop size in the 650,000 - 680,000 MT range. The California Agricultural Statistics Service (CASS) Objective Estimate, will be released in early September. This estimate will provide further clarity for the overall crop size and average nut size for this year.

As is typical with early harvest indications, there have been a number of issues raised by walnut growers and processors of which the extent of impact remains to be seen. These include a frost during the early spring which caused some growers anxiety as they projected a much smaller crop. More recently though, a wind event in the northern growing regions caused widespread broken branches. Many growers there are now reporting that this damage is due to a much larger volume of walnuts, and larger average nut sizes weighing down their trees this summer, with some growers even reportedly discussing pre-mature pruning activity in order to mitigate further damage to their walnut orchards. Thus, what was once thought to be a new crop in jeopardy is now estimated to be an almost overly robust and healthy crop.

The CASS Objective Estimate, which will be released in early September will be relied on by many buyers and sellers as the benchmark to determine opening prices.

Howard, Hartley, Bleached Hartley, Tulare, Vina, and Serr varieties of inshell walnut will be harvested first, with Chandler quick to follow. We are currently marketing new crop inshell Jumbo and Jumbo / Large Chandler Walnuts, please let us know your requirements

The latest monthly shipment figures from the Raisin Administrative Committee (RAC) showed California raisin shipments down 39% in June compared to the prior year. The damage caused by lower bunch counts and two rain events during the harvest clearly compromised California’s supply continuity for many customers. Major buyers around the world, including in the U.S., are covering with raisins from Chile or South Africa given the absence of suitable fruit from California until new crop shipments in September / October.

Due to the short crop last year, we are seeing earlier interest from large foreign buyers looking to secure their forward needs. Since the field price paid to growers by processors has not yet been established, some packers are holding off on firm offers until around September while others are already booking forward contracts for the new crop.