May 27

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world.

World Tour: Thoughts and Observations

Anderson Exports is back in the United States after a 36 day trip from Los Angeles, California through Asia and Europe, visiting current customers, prospecting new business, and ending with a week alongside the INC in Seville, Spain.

Asia's Rising Tide

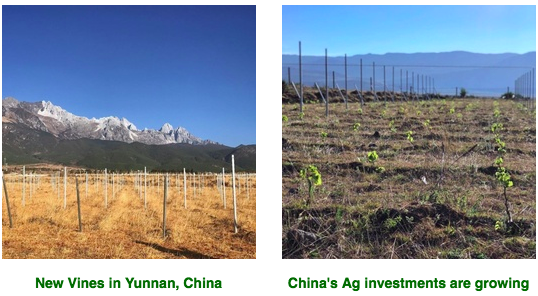

There are many notable trends to discuss after visiting with our contacts from around the globe. Most obvious is the rising wave of Asian economic relevance. Not only is China growing in importance by the day for California exporters, it is also planting many new hectares of land for vine fruit, tree nuts, and other tree fruits.

An indication of China’s growing agricultural sophistication and changing consumer tastes came from a good friend of ours in Shanghai, who recently purchased land to start a vineyard in Yunnan province. Napa or French quality Chinese wine is the goal, as evidenced by the fact LVMH, the parent group of Louis Vuitton and many other luxury brands, purchased the land adjacent to our good friend’s new vineyard to start a winery of their own. This is clear evidence that the tastes and financial power of China’s middle class are real and growing. China, with 4 times as many people as the United States, needs only to become ¼ as rich as the US per capita to take the lead as the World’s largest economy. If LVMH is investing in local, vertically integrated luxury supply in rural China, you can be sure there is ample demand. We have some photos of new vines in Yunnan below:

As became increasingly clear to us throughout Asia, China is not the only economic power to take note of. One surprising statistic we learned in Manila is that the Philippines has one of the fastest growing number of Ultra-High Net Worth individuals, a number which is expected to double by 2022. With 110 million people, 10% live and work abroad, which adds up to several billion foreign dollars pouring back into the Philippines each month. Further, many US and European based customer service related call centers are being relocated to Manila, creating lots of new opportunity in real estate and good jobs for those with English as a Second Language (ESL) education.

There is no doubt that the rising middle class of China will be one of the most important economic drivers of our future business as an exporter, but we are also convinced of the economic importance of the APEC (Asian Pacific Economic Cooperation) countries as a whole.

As we are in the business of food, it is important to think in terms of people, and more people live in this relatively small area of the world than outside it. You can see the scale of this statement clearly in the image below:

More people live inside this yellow circle than outside of it. This is Anderson Exports’ primary area of focus for developing new business over the next 3 - 5 years.

Europe and INC

Our final insight we will provide from this trip is the growing competition in the UK and EU caused by discount supermarkets. Paradoxically, despite all the EU’s stringent requirements on imports for nuts and dried fruits, it seems the lowest price possible is the only purchasing requirement in these regions today.

Further, upon visiting Seville during the International Nut Congress (INC), we learned that the largest represented group at the INC this year was from Turkey. A notable change as compared to past INCs, as Turkish Sultanas and other dried fruits & nuts have become the primary source for the UK and EU as their supermarkets and importers remain in downward price competition. Further, with the realities brought by the Brexit vote, it seems citizens of the UK are tightening their belts and saving more than last year. A trend that will continue to support the importing of low-cost origins for dried fruits & nuts.

As a young company ourselves, visiting the INC we did not see much room to expand into the European markets within the next 3 - 5 years, as many cartels...ahem, buyers and suppliers, have long established relationships.

We do see massive potential to expand into these markets after this 3 - 5 year timeline though, as many of the elder Patriarchs of the industry will be retiring and handing off their businesses to their successors, who will be in need of forging their own lasting supply relationships.

The Plaza de Espana and the INC's Final Dinner

Raisins

California raisins are too expensive and not high enough quality to warrant much interest from many buyers until the new crop is available. We expect a much lower carry-out this year due to the weather damage and resulting crop shortage. Lower carry-in to the next year will make the development of the new crop especially important for the total supply picture. We expect bunch count readings in the coming month to provide some early indications.

Turkish raisins picked up market share this year due to high prices and unreliable quality out of California. Turkish origin raisins are also attractive to global buyers due to supply continuity: Turkey’s crop is large enough to ship throughout the year while Chile’s crop is not. Processing improvements, close proximity to key export markets, and lower relative prices to other origins are robust advantages for Turkey’s raisin industry.

Chilean raisin prices opened high post-harvest amid elevated prices out of California but have softened recently. Quality on body/flesh, color, taste, and sugar content is viewed as good in general this year. Chilean grapes are produced for the fresh fruit export market then producers sell remaining fruit to the wine, fresh fruit, and raisin industries. Due to these dynamics, there is a higher share of jumbo raisins (~70%) compared to medium raisins (~30%). Chilean Thompsons are selling out more quickly than Flames, particularly in the medium sizes.

We are well-positioned to offer Turkish raisins on a spot and forward basis as well as California and Chile material and welcome your inquiries.

Cranberries

Early procurement planning is in focus as lead times lengthen and prices rise for sweetened dried cranberries (SDCs). Supply has been constrained due to shorter crops and regulatory actions while global demand appetite has been strong. At the beginning of 2018, the U.S. and Canadian crops registered year-over-year declines of 18% and 25%, respectively. The USDA approved a 15% handler withholding and may approve further supply reductions for the coming years, compounding the already tight supply for cranberries. In Taiwan and South Korea, we observed makers of breads and mixes switching out raisins in favor of cranberries due to the higher relative price of raisins. Global demand has been strong and we believe there is some substitution-driven demand due to high prices of California raisins which may subside as raisin prices ease when the new crop comes online.

Since there is no spot material available for prompt shipment, we advise our buyers to plan in advance for their forward needs since supply-side constraints are unlikely to subside soon. We are now offering contracts for shipment in August - December 2018 and expect 2018 material to be fully booked in the coming months. This pace of bookings will require buyers to act much earlier than in the past to secure forward material, particularly for 2019 shipments. Moreover, buyers with sticker shock should recall prices have been even higher than current levels in past years and that USDA crop withholding decisions expected in June may drive prices even higher for 2018 and 2019 material.

Walnuts

The new crop in California is developing well so far. The Subjective Estimate Report should provide an early indication of the crop size. Some California packers are selling completely out of some shelled sizes. Some growers that decided to hold on to in-shell loads in the hopes of higher prices which failed to materialize are now off-loading some material into the market. We are well positioned on in-shell Chandler needs.

Brazil Sugar

International sugar prices have firmed since mid-May due to nationwide protests in Brazil against high diesel prices and other factors. Output growth in key growing regions including India, Thailand, and the EU continue to drive the global surplus in sugar. For the 2017/2018 season, India crossed 32mmt and Thailand achieved 14.6mmt, reflecting major increases over the year prior.

We offer Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 100,000mt) or forward contract basis including long-term contracts of 300,000mt / month x 12 months. Payment by SBLC, BG, or DLC from global top 50 bank.

German Beet Sugar & Thai Sugar

The European Union’s importance in the global sugar trade is increasing after production quotas and price guarantees expired in October 2017. With close proximity to key export markets, the EU is expected to become a net exporter for the first time in more than a decade. Germany’s beet sugar crop, which commands a premium over other growing regions, is also benefiting from increased planted acreage and favorable weather.

We offer German Beet Sugar & Thai Sugar by the container (MOQ: 10 FCLs) and welcome your inquiries.

Brazil Soybeans

Exporters of Brazil soybeans are actively monitoring the potential impact of a strike by independent Brazilian truck drivers. Despite beginning a few days ago, supply chain disruptions are already being felt in the meat sector where blockages and delays are causing unforseen costs. With approximately 30% of the 2017/2018 soybean crop awaiting shipment from Mato Grasso, exporters are keen to move this product ahead of the safrinha corn harvest which begins next month.

We supply GMO and Non-GMO certified soybean from Brazil. MOQ: 100,000+ tons. Payment by SBLC, BG, or DLC from global top 50 bank.

Brazil Corn

After weeks of dry weather in southern Brazil, thunderstorms hit the region and caused damage to the safrinha corn crop. In addition to the prolonged dryness and storm damage, a short period of cold temperatures recorded as the coldest of the fall season so far also impaired the development of the crop. Such adverse weather events are dragging estimates for the Brazil corn crop lower.

We supply GMO and Non-GMO certified corn from Brazil. MOQ: 100,000+ tons. Payment by SBLC, BG, or DLC from global top 50 bank.