July 1, 2018

Anderson Exports is a Bulk Ingredients Sourcing Agency in Northern California. We specialize in sourcing the best ingredients from California, Brazil and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

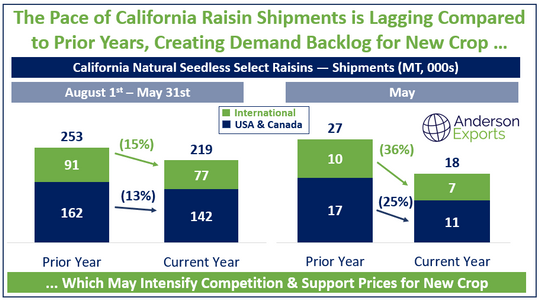

Raisins

Based on data from the Raisin Administrative Committee (RAC), shipments of California Natural Seedless Thompson raisins are down considerably compared to the prior year. From the beginning of August to the end of May, total domestic & international shipments are down 13% this year compared to last. This May alone, total shipments were down a staggering 32% compared to last May. Based on these substantially lower shipments, particularly for the recent and coming months, a backlog of demand is building. We expect the pent up demand for California raisins to impact opening prices even if the total crop size returns to a more normal level.

The new crop is looking good with bunch counts up considerably from last year. Fingers crossed for no major weather events this year. New crop shipments should begin around October. September is possible if there's an early harvest but planning on October is more reasonable. Current crop is virtually sold-out across the Central Valley of California. Given the adverse weather events and the resulting quality concerns, we're advising our clients to cover current needs with Chile at the moment and stay away from the rain-related issues with the current crop of California raisins.

While this past year has proved to be one of the most challenging in decades for the California raisin industry, California raisins are the highest quality available in the world. Even with the damage to the crop, import shipments from some of the highest spec. countries increased year-over-year. For example, Japan's year-to-date imports of California Natural Seedless raisins are up 17% compared to the prior year period. Unprecedented weather events surely presented challenges to the California raisin industry this year. However, the California raisin industry is an exceptional and resilient one which will continue to be a world leader in quality and supply continuity in the years ahead. We are now engaging with clients for forward contracts on California raisins for upcoming crop and look forward to serving your needs.

Chilean raisin suppliers still have stocks available at relatively attractive price levels compared to their Californian counterparts and we welcome your inquiries.

Cranberries

Shortages of fruit and high prices persisted in recent weeks amid strong global demand and smaller crops from both Canada and the US. The spot market for sweetened dried cranberries (SDCs) has disappeared since suppliers have no free production slots for the next few months. Therefore, buyers are strongly advised to plan longer in advance to fill their SDC needs. We are currently offering forward contracts on SDCs and welcome your inquiries.

Walnuts

The California Walnut Board shipment data for May showed lower shipments of In-Shell and Shelled material compared to the prior year. From the beginning of September to the end of May, shipments of California in-shell and shelled walnuts are down 25% and 6%, respectively, compared to the prior year period. Based on the severe heat during the summer months last year, walnut processors opted to shell much more material than normal so the substantial decrease in in-shell shipments is understable with this in mind. Focus now turns to the development of the new crop and total production estimates which should begin to come into view in the coming months. While California packers are comfortably sold, there are some in-shell and shelled loads available and we welcome your inquiries.

Almonds

The Objective Estimate for the new Almond crop is scheduled to be released on July 5th, which should provide further clarity on size expectations for the new crop. In recent months, there have been some concerns about frost damage to trees but with much time to pass still before the harvest, market activity has been understandably quiet. Prices remain high and supplies tight in many varieties and sizes. We anticipate the pace of new crop contract discussions to gain some traction after the Objective Estimate releases this week.

Sugar

The volume of sugarcane crushed in the last two weeks of May in Brazil’s Central / Southern regions is estimated at 32.9 million metric conts (MMT) which is down 23% from the previous two week period. The trucker strike and resulting paralysis to the transportation of sugar is primarily to blame for the drop-off. Depending on how the coming weeks progress, the industry may stage a recovery but any further labor troubles will surely be costly.

Due to the relative profitability of ethanol vs. sugar in the current environment, the proportion of cane directed to sugar production is reaching record low levels, dragging further on total sugar output available for export. For example, in Brazil’s Central / Southern regions, the share of cane destined for sugar production was approx. 34% in May, down considerably from 47% a year ago. This is the lowest share of cane directed to sugar production in over 20 years.

To be sure, a higher share of cane would be directed to sugar production if prices were higher. However, due to large production increases from key regions, this situation of global oversupply is unlikely to subside soon. Sugar production in India has surged 60% year-on-year for the 2017 / 2018 season.

We supply Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 100,000 MT) or forward contract basis including long-term contracts of 300,000 MT / month x 12 months. Payment by SBLC, BG, or DLC from global top 50 bank.

Beet Sugar

n the European Union, high temperatures and dryness weighed on yields for many crops in recent weeks but have not yet dragged on sugar beet yields. The May yield reading for European sugar beets was up approx. 2% from the 5-year average compared to European rye which is down approx. 2.5%. Sugar beet crops in the EU for the 2018 / 2019 season and beyond may experience downward yield pressure as the EU moves to ban pesticides. The pesticide protects beets from ground and air pests so sugar beet farmers will need to find alternatives. The insecticide ban is expected to decrease production by approx. 1.25 MMT in the EU for the 2018 / 2019 crop.

We supply German Beet Sugar (MOQ: 1 FCL) as well as Thai Sugar (MOQ: 10 FCLs)

Brazil Soybeans

Lingering transportation problems from the trucker strike continued to interfere with Brazil’s soybean market in recent weeks. Due to the much higher freight rates resulting from the strike resolution agreement, many buyers have been on the sidelines. These issues are disrupting the movement of soybeans to the port for export.

The recent protest-related bottlenecks have created unexpected headwinds to Brazil’s soybean industry which is otherwise well-positioned to take market share from other key growing regions, especially the US. Elevated trade tensions between the Trump and Xi Jinping, have raised the potential for a 25% tariff on US soybeans destined for China. Unless trade tensions ease soon, the US will likely become a less important supplier of soybeans to China. In 2017, the US represented approx. 33 MMT, or just over one third, of China’s total soybean imports of 95 MMT in 2017. South America, which produces nearly 50% of global soybean output, will likely see more interest from Chinese buyers. In particular, Brazil will be well-positioned to pick-up incremental tonnage since Argentina has been hindered by adverse weather conditions. Of course, Brazil’s ability to benefit from these conditions depends critically on the efficacy of the country’s transportation networks and favorable labor relations so global buyers will be monitoring these issues closely in the weeks ahead.

We supply GMO and Non-GMO certified Soybeans from Brazil. MOQ: 100,000+ MT. Payment by SBLC, BG, or DLC from global top 50 bank.

Brazil Corn

Estimates for Brazil’s safrinha corn production fell considerably in recent weeks. Current estimates for the 2017 / 2018 safrinha corn production are ~55 MMT, down 19% from 68 MMT in the prior year. Planted corn acreage declined year-over-year due to low corn prices and delayed planting. Adverse weather conditions also dragged on production figures. Some Northern regions went over 40 days without rain, indicating the severity of the dryness problem. Severe storms and powerful winds also blew down corn stalks, adding further damage from adverse weather. Brazil’s total corn production is estimated at approx. 82 MMT, which is down approx. 17% from the prior year figure of 99 MMT.

We supply GMO and Non-GMO certified Corn from Brazil. MOQ: 50,000 MT. Payment by SBLC, BG, or DLC from global top 50 bank.

Work With Us As a Supplier

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.

Introducing voyage-x.com

voyage-x.com, a digital marketplace for containerized bulk food & beverage products, is now live.

voyage-x.com is a one-stop shop for global food procurement with thousands of products spanning from bulk ingredients to consumer packaged food and beverage products.

We welcome your inquiries and look forward to working together to deliver you the highest quality ingredients from the world's best suppliers. We are available to our suppliers and buyers 24/7 over email, phone, or WhatsApp.