June 10

Anderson Exports is a Bulk Food Sourcing Agency in California specializing in supplying quality ingredients from California, Brazil, and the rest of the world. Our newsletter delivers actionable market intelligence to inform our clients' purchasing decisions.

Walnuts

The California walnut acreage report released last month showed that in 2017, bearing acreage rose to 335,000 acres. In terms of year-over-year change, this is the largest increase for bearing acreage on a growth percentage and acres-added basis over the last 10 years.

Prices are softening for California material and many suppliers are reaching comfortably sold territory in several varieties and sizes. In this environment, we have seen buyers with the ability to close quickly snap up spot loads at attractive prices with suppliers looking to liquidate their last loads in particular kernel sizes. We are well-positioned in kernel and also have some in-shell Chandler available and welcome your inquiries. Though the new crop is still a ways away, we are beginning to offer new crop contracts for California walnuts.

The Chilean walnut crop this year is widely considered to be good quality. Since Chilean material opened when California prices were sky high due to heat-related damage, there has been a major price correction in the market recently. For Chilean In-shell 30MM+, we’ve seen prices come down from USD $1.91 / lb ($4.20 / kg) to $1.63 / lb. ($3.60 / kg), a decrease of 86%. Now that prices have dropped, we’re seeing buyers coming in to close big volumes for in-shell, hand-cracked, and machine-cracked Chilean material.

Dessicated Coconut

Indonesian dessicated coconut prices declined between the 4th quarter of 2017 and the start of Ramadan. Prices were high in September/October 2017 and nearly matched prices from the Philippines, motivating Indonesian factories to sell off as much stock as possible before the start of the fasting month. Although suppliers were abundant, weak demand from the Middle East, Eastern Europe, and South America pushed prices lower. With prices at such depressed levels, many Indonesian factories are opting to cut production shifts rather than operate at full capacity which also coincides with the month of Ramadan, during which workers tend to work fewer hours anyway. We expect coconut harvesting to slow during the monsoon season in July/August, which may temporarily tighten supply availability in Indonesia.

In the Philippines, coconut factories are almost sold out for 3rd quarter 2018 shipments, besides a few odd containers available. Weak demand from Western Europe and the USA combined with the good harvest in the Philippines last year have weakened prices since the beginning of 2018. We expect the upcoming typhoon season to disrupt the harvest, though the extent of damage and effect on prices remain to be seen. Also in focus for the post-Ramadan period will be the strength of Chinese demand for raw coconuts and by-products like dessicated coconuts and coconut milk. Prices may firm rapidly if adverse weather and strong chinese demand coincide in the coming months.

South African Pecans

South African pecan farmers benefited from favorable weather for the 2018 crop. Early nut set figures demonstrated the good health of the crop. Encouraged by high global prices, South African farmers are planting new pecan orchards at a rapid pace. The upcoming crop is expected to be another record pecan crop for the country. The South African pecan crop consists primarily of Wichita, Choctaw and Barton varieties. South Africa’s Oversized Wichita Pecans are particularly favored by Asian buyers.

In the years ahead, we expect the South African pecan crop to be increasingly sought after by global buyers. To be sure, at present, the South African crop (~16,500 MT) is a mere fraction of other key growing regions -- namely, the United States (~125,830 MT) and Mexico (102,060 MT) -- for the 2017 / 2018 crop. Droughts also affected the crops in 2015 and 2016. With time, however, the rapid orchard plantings over recent years will start to produce. The industry will likely also invest in new processing equipment to meet strict shelled spec needs, capturing value-add currently forgone by selling primarily in-shell.

With on-the-ground experience in South Africa’s key pecan growing regions, we are well positioned to fulfill your needs, particularly on Fancy Junior Mammoth Halves & Fancy Mammoth Halves.

Raisins

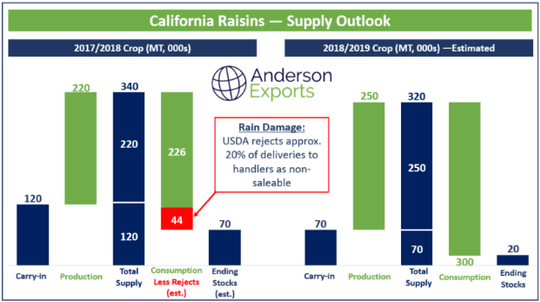

With the new crop drawing in California closer, we are beginning to offer forward contracts. Due to the rain damage during the harvest and current price levels, we would advise waiting for new crop or sourcing from Turkey or Chile. Chilean prices have softened somewhat in recent weeks and we are well-positioned to fill your needs though material will not last long. Turkish raisins are also good quality and we welcome your inquiries.

Cranberries

Prices for sweetened dried cranberries (SDCs) remained firm in recent weeks as shortages continue. With shorter crops in both the U.S. and Canada this year and handler withholdings removing further material, supplies are tight and lead-times are long. The next USDA crop withholding decision is expected in June which may compound the situation. We are currently offering contracts for shipment in August - December 2018. There is no material available for prompt shipment. Buyers with forward needs are strongly advised to plan early in advance to secure material as the spot market for prompt deliveries of SDCs is non-existent due to severe shortages of fruit.

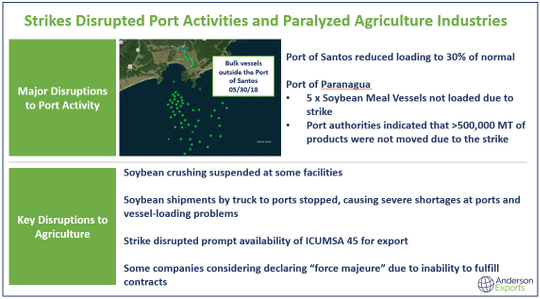

Truck Driver Strike Disrupts Brazil Agriculture Sector

An extended period of dry conditions in Center and Southern Brazil is dragging down estimates for sugar production in the region. Soil moisture is extremely low in some areas which creates adverse growing conditions and lower sugar cane yields.

In protest of rapidly rising fuel prices, Brazilian truck drivers brought the transportation network of the nation to a grinding stop. Beginning on May 9th, workers took to the streets, barricading key highways and obstructing port entries. Within days, nearly every single gas station in Rio ran out of fuel and severe shortages of food and other products spread across the country. Livestock producers ran out of feed for animals and had no choice but to cull millions of animals. Dairy farmers dumped milk and supermarkets sold out of perishable foods.

In the Agriculture industry, soybean shipments to ports stopped and soybean crushing came to a halt due to the transportation gridlock. At the Port of Santos, loading plummeted to 30% of normal and at the Port of Paranaguá, over 500,000 MT of products were not moved due to the strike. In the sugar industry, the strike compromised the prompt availability of ICUMSA 45 for export.

We supply Brazil origin ICUMSA 45 Sugar by the vessel on a spot (MOQ: 100,000 MT) or forward contract basis including long-term contracts of 300,000 MT / month x 12 months. Payment by SBLC, BG, or DLC from global top 50 bank.

We also supply German Beet Sugar (MOQ: 1 FCL) and Thai Sugar (MOQ: 10 FCLs)

Brazil Soybeans & Corn

Exporters of Brazil soybeans and Corn are hoping to resume to normal operations after the disruptive truck driver strikes. After weeks of dry weather in southern Brazil, thunderstorms hit the region and caused damage to the safrinha corn crop. In addition to the prolonged dryness and storm damage, a short period of cold temperatures recorded as the coldest of the fall season so far also impaired the development of the crop. Such adverse weather events are dragging estimates for the Brazil corn crop lower.

We supply GMO and Non-GMO certified Soybean and Corn from Brazil. MOQ: 100,000+ MT. Payment by SBLC, BG, or DLC from global top 50 bank.

Rice

We also offer a wide range of rice products including: Gaba Jasmine, Thai Fragrant, Thai Hommali, Thai Black, Thai White, Thai Red, and Thai Parboiled Rices. Payment by SBLC or BG.

Work With Us As a Supplier

We are always looking to grow our supplier base with companies capable of delivering continuous high quality product at large volumes. If you are interested, please reach out and introduce yourself.